The Sunday Mail

Persistence Gwanyanya

SIX years after emerging from a decade of economic challenges, Zimbabwe is now on the recovery path.

Since the last quarter of 2011, the economy has been slowing down as both global and local influences take toll.

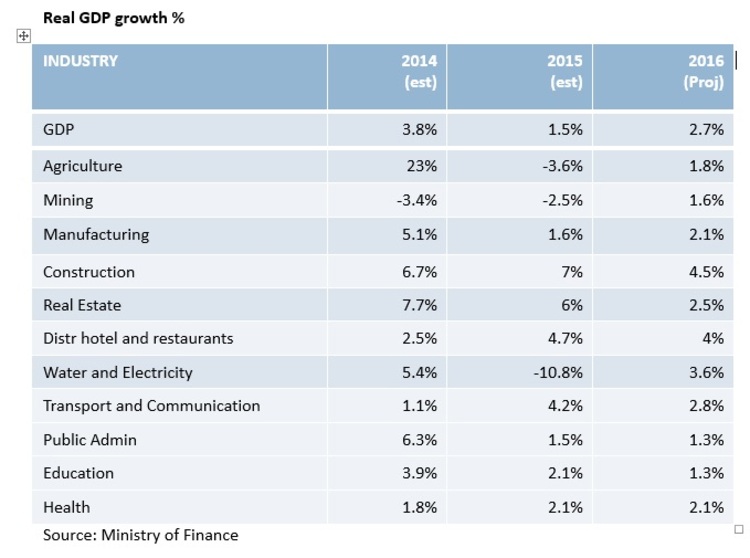

The economy is now expected to grow at the slowest pace of 1,5 percent since dollarisation, a downward revision from the initial projection of 3,2 percent.

A moderate growth of 2,7 percent is projected for 2016.

Downward risks to the global economy appear more pronounced as they did just a few months ago.

Global growth for 2015 is now projected at 3,1 percent from prior year growth of 3,4 percent and the World Economic Outlook July 2015 forecast of 3,3 percent.

Modest recovery in advanced economies, coupled with five consecutive years of slowdown in emerging markets suggest that the medium and long-term economic forces are at play.

The long term global growth will be sluggish as economies try to rebalance.

Economic rebalancing will be pronounced in China as it reduces its investment and exports whilst promoting domestic consumption.

China is now expected to grow at seven percent per annum, which is the slowest pace since the new millennium.

Slowdown in China and other emerging economies coupled with weak economic and financial conditions in the European countries has had negative ramifications on global commodities prices.

Real commodities’ prices, notably those of metals, have fallen from their peak of 2011 to historic lows after the financial volatility which started in mid-August this year.

Table – World growth estimates adopted from The World Economic Outlook, October 2015 update*

Weaker commodity prices have had negative ramifications on commodity dependent Zimbabwe.

Seven primary products, dominated by precious and semi-precious metals namely gold, tobacco, nickel ores and concentrates, ferrochrome and industrial diamonds contributed 70 percent of the country’s exports for the 10 months to October 2015, thereby demonstrating how vulnerable the economy is to commodity price fluctuations.

Weaker commodity prices and reduced financial flows to emerging markets saw deeper currency depreciation in commodity exporting countries and emerging markets.

Of particular note is the rand which lost over 13 percent in value against the US dollar since January 2015.

The depreciating rand has worsened the country’s competitiveness by making the cost of doing business in Zimbabwe higher than in trading partners. Ideally, the cost effect of an appreciating currency would be compensated with increases in productivity to remain competitive, which in not the case in Zimbabwe.

The appreciating United States dollar came on the backdrop of an overvalued currency in Zimbabwe. It is estimated that the US dollar is 45 percent overvalued in Zimbabwe, making it a high cost and less competitive country.

This has seen the country being ranked 124 out of 145 countries on competitiveness by the World Economic Forum this year.

Prior to dollarisation, the country would sort out its competitiveness issues by devaluing its currency. This option is no longer available under dollarisation as exchange rate is now determined externally.

The competitiveness challenges are reflected in the country’s deteriorating BOP position.

In 2015 a trade deficit of US$2,9billion (2014:US$2,7billion) is projected from imports of US$6,3billion and exports of US$3,4billion.

This is an unsustainable situation as it has negative consequences on the already precarious liquidity situation in the country.

Given limited policy options, the country is stuck between internal austerity, like in the EU countries, and general price reduction.

Deflation of 1,6 percent is projected by the end of the year and deflation risk remains high in the outlook period as tight economic and financial conditions continue.

Internal austerity could take the form of reducing both public and private sector expenditure and restructuring the public enterprises.

However, current expenditures, specifically wages, continue to take the greater chunk of Government’s budget, which largely demonstrates structural challenges in the economy, including a bloated civil service and underperforming parastatals.

This year we are going to experience a budget deficit of US$150million mainly to fund civil servants bonuses and pay arrears to international financial institutions.

This deficit will be funded largely through borrowing on the domestic market, with crowding out effects to the private sector.

To generate meaningful growth, there is need to trim the civil service and reduce their share of budget from 80 percent to 40 percent in line IMF Staff Monitored Programme recommendations.

Measures to manage the wage bill have already been spelt out and Finance and Economic Development Minister Patrick Chinamasa indicated that Cabinet has approved the move. This is expected to produce savings of US$170,4million per annum.

Government’s commitment to enforce a code of corporate governance on public and state enterprises is a good gesture but there is need for boldness in implementing the same.

Austerity measures are not without their short to medium term costs.

Cutting the civil service will worsen unemployment levels and will have deeper socio-economic effects in the long term such as increased informalisation of the economy.

The informal sector in Zimbabwe is a low productivity sector, which is very uncompetitive and a non-tax paying drag on development.

This demonstrates the extent to which the growth should balance the virtues of demand management, economic policies (austerity) and supply factors which encompasses increasing investment and productivity. This means savings will not be enough to generate the desired growth.

Even if the target of 40 percent current expenditure as a share of budget is achieved, it may not be enough to spur meaningful growth in Zimbabwe given infrastructure deficit and the need for industry to retool.

There is therefore need for significant FDI inflows to generate desired growth. No wonder why this is the thrust of the 2016 budget.

A country with an infrastructure deficit of US$14 billion to US$20billion and budgeting for only US$237million on capital expenditure definitely needs some significant FDI inflows. The current FDI inflows remain low although they are improving yearly.

An estimated, US$614 billion is projected this year up from the 2015 budget estimate of UDS$591million.

By its nature FDI is not a market determined flow, it is determined by factors other than interest rates.

The ease of doing business factors are important influences of FDI.

It is delighting to note that frantic efforts to improve the ease of doing business in Zimbabwe continue to reflect in the improvement in World rankings from 171 in 2015 to 155 out of 188 countries in 2016. However, the Indigenisation and Economic Empowerment Act continues to be a major deterrent to FDI flows. We will wait until the Christmas to see what amendments will be made to the Act, hopefully these will be palatable with the efforts to attract FDI.

At the same time, FDI alone is not the panacea to the country’s economic challenges.

There is need to sort out the debt overhang estimated at US$8,34billion and negotiate with its financiers for debt restructuring or rescheduling.

Consistent with this strategy, Government has negotiated with its international financial creditors to clear arrears with the IMF, World Bank and African Development Bank amounting to about US$1,8billion by June 30, 2016 as per the Lima agreement. Recently, we have seen the World Bank warming up to re-engagement moves and has already started some discussions with some local private players. If Government successfully pays its arrears as promised, there is scope for reassessment of the country’s risk profile and credit rating, which is important for attracting cheap credit at better terms.

At the moment, Zimbabwe has no capacity to continue contracting expensive short debt. The risk of getting into a debt trap is high and history has taught us that once a country gets into this trap, it will be difficult to get out of it.

In a nutshell, the economic outlook remains weak, but much will depend on the developments in the global economic front. FDI inflows can be a game-changer. As much as debt restructuring is welcome, it is important to note that debt is not a sustainable growth path.

History has shown that a country that saves can use its capital better and will grow faster at a sustained rate.

Persistence Gwanyanya is an economist and banker. He is also a member of the Zimbabwe Economic Society. He writes in his personal capacity and this article does not represent the views of his employer